Written by Adnan Ali Amir

Pricing effectively within an ever-changing reinsurance landscape

3 minutes

See the key drivers for digital transformations within the reinsurance sector and why pricing has established itself as a key initiative for successful reinsurers.

January 2023 presented a unique inflection point for the reinsurance sector. With a fierce renewal season and an imbalance in the demand and supply of capacity tipped in favour of reinsurers, many were able to reap favourable results after years of sub-par returns.

The geopolitical and macroeconomic factors that affected global reinsurance markets included the war in Ukraine, 40-year high inflation, recessionary fears, fractured energy markets, increased interest rates, and Hurricane Ian, the second-largest insurance loss on record after Hurricane Katrina. The result of all this was a significantly volatile market and pricing increases seen in the January 2023 renewal cycle.

However, the renewal season wasn't all smiles for reinsurers. Year-end 2022 saw the reinsurance market experience the largest capital squeeze ($66bn) since 2008, restricting reinsurers' abilities to maximise profitability during their peak season. Although there was an expectation that more capital would arrive, this was not the case. This reduced capacity will increase reinsurers' dependence on digital transformations to ensure efficiency in risk pricing and promote revenues.

The International Monetary Fund (IMF) expects the global economic uncertainty to continue well into the year, and reinsurers that can successfully leverage the ensuing hardening market will be best positioned to lead the market for the future.

The next part of this blog will explore the key drivers for digital transformations within the insurance sector and why pricing has established itself as a key initiative for successful reinsurers.

Loss ratio improvements

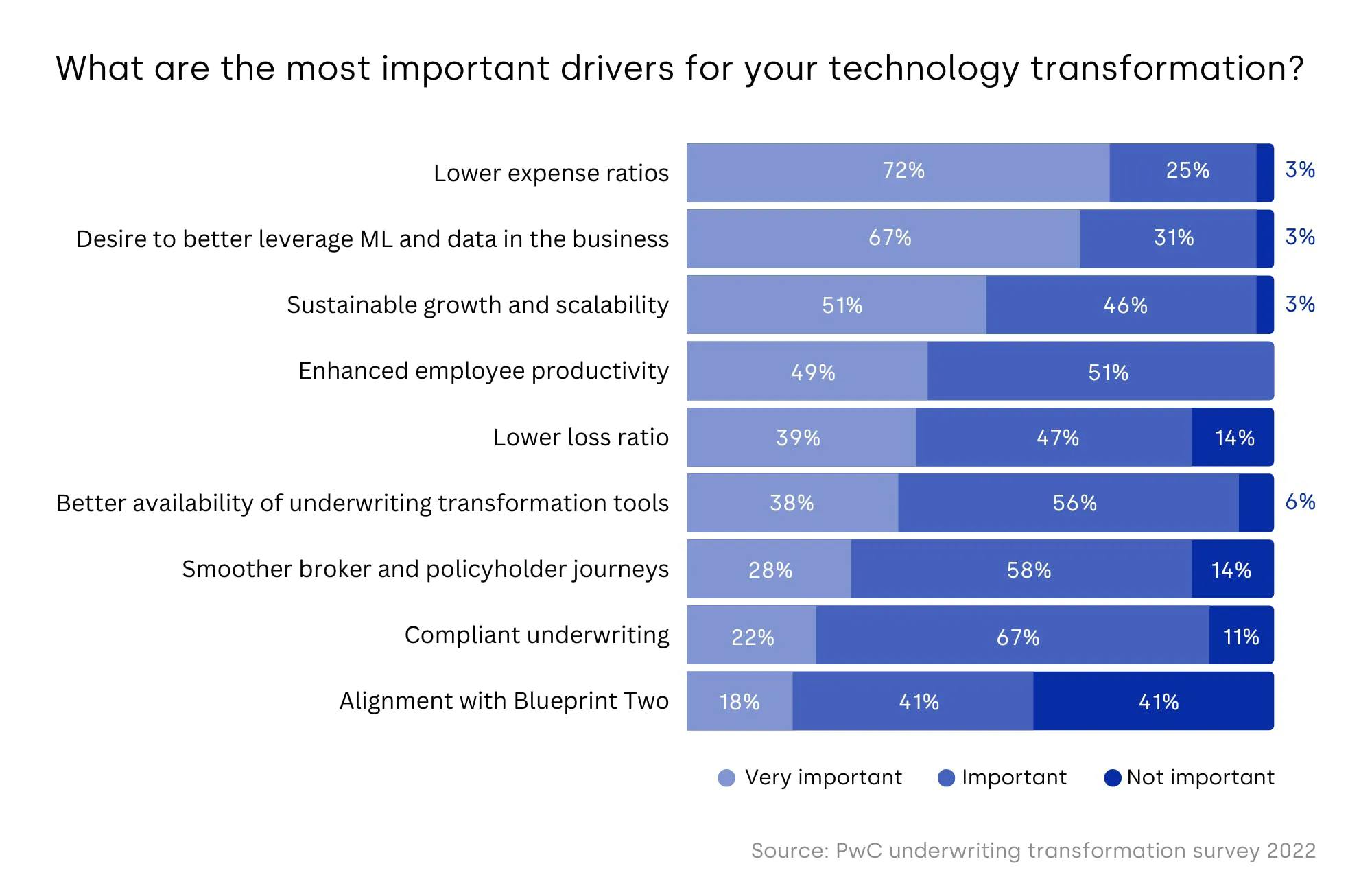

The combined (loss and expense) ratio is a crucial measure of profitability for insurers. According to PwC's top five drivers of technology transformation, nearly all senior leaders recognize the importance of lowering both, with 97% seeking to reduce expense ratios and 86% reporting lowering loss ratios as important or very important.

Lloyd’s and London Market expense ratios are typically around 10% (once brokerage is stripped out), compared with loss ratios that can be greater than 60%. This means that a 2% impact on the loss ratio will have a six times larger impact on an insurer’s profitability than the same 2% movement on their expense ratio.

Reducing expense ratios may seem like an easier solution, but pricing and underwriting transformation has the potential to generate material improvements in profitability through loss ratio improvements and, as such, generate significantly greater profit than other programmes focused on expense saving alone.

Furthermore, a poll hyperexponential conducted at GIRO 2022, the UK's premier actuarial conference, unveiled compelling poll results that revealed why pricing transformations are top of mind for many in the industry. Actuaries present reported average expectations of 2.8%pt improvement to their firm's loss ratios through investment in better pricing data and models.

Doing more with the data available to reinsurers

For decades, reinsurers have been limited by the data that is made available to them from their insurance partner(s). This problem is further exacerbated by the reinsurance industry's reliance on spreadsheets, hindering its ability to price with the cutting-edge capabilities needed to succeed in a rapidly changing market. This dependence coupled with limited data often leads to errors, inaccuracies, and discrepancies.

Within a hardening reinsurance market, pricing agility and intelligence will be key differentiators for forward looking reinsurers. Pricing technology helps reinsurers do more with the data made available to them and creates benefits like data-driven decision making and real-time portfolio analytics.

Data-driven decision making at the time of making risk assessments

The ability to analyse portfolios in real-time enables reinsurers to maximise the dynamic insights that they can derive. This in turn, empowers them with the ability to make data-driven decisions at the time of making risk assessments.

Benchmarking risks against each other across the portfolio is empowering reinsurers with the ability to make choices that best fit their strategic imperatives. These include assessing the level of diversification and marginal impact of the risks being analysed.

Reinsurers that make best use of the data made available to them will be best poised to succeed as we enter a hardening market.

In conclusion

The complexities reinsurers face, and the potential upside, make now the best time to invest in pricing transformations. As the market evolves, reinsurers that can react quickly and make data-driven decisions will be ahead of the pack.

At hyperexponential, we meet the reinsurance industry's need for pricing agility and help reinsurers unlock value at every step of the pricing value chain. Our next-generation pricing platform, Renew, is enabling data-driven decision-making and maximising profitability for reinsurers across the globe, including leading reinsurers like Convex, Conduit Re, and more.

To learn more about how hx Renew has enabled high-growth reinsurers unlock access to data insights, refine actuarial and underwriting processes, enable automation at scale and achieve loss ratio benefits, get in touch with our team today.