Market trends

Going all the way: what is an agentic underwriting workbench and why does it matter?

Amrit Santhirasenan

A big technology shift has been underway over the last two years. It's about to hit insurance.

In all industries, the "workbench" that professionals have been using, often for decades, is being completely redefined by AI. The popular example right now is law: drafting, diligence, citation, and matter management have all moved inside a new kind of system - one in which agents do the work and lawyers direct it. (The co-founder of Harvey captured the shift well in a recent blog entitled "Legal is Next".)

Interestingly, software engineering was one of the first sectors to be impacted by this shift. Customer support followed the same pattern, as have countless other disciplines. Each time, the work itself migrated into the software. Before, the humans used a disparate set of tools to do their jobs and the workbench connected everything together; now the work is driven by AI agents and orchestrated inside the workbench:

Underwriting is next. It's clear that the next workbench for underwriting is going to be an agentic environment: an agentic underwriting workbench.

Here's what it is, why it matters, and why neither first-generation AI nor the foundation models alone will get you there.

What an agentic underwriting workbench is

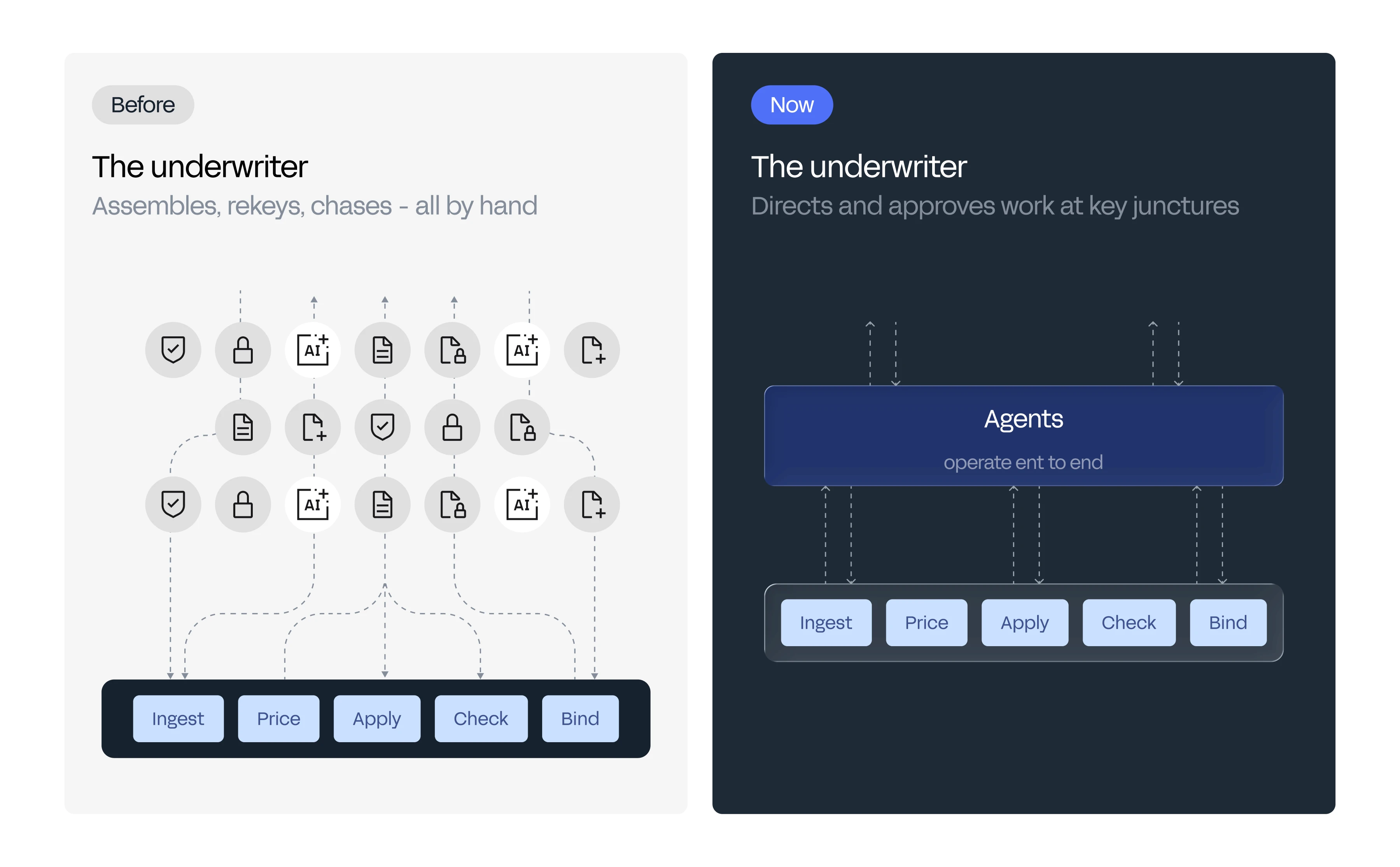

The traditional underwriting workbench was the best system for the job when the system couldn't actually do the job. It was the place people collected submissions, routed them to others, recorded what they did with them, and stored the artifacts at the end. Whatever made the underwriting decision 'good' (appetite, pricing logic, portfolio context, exception handling, organizational conventions) lived outside the workbench: in spreadsheets, emails, underwriting notes, and people's heads.

One of the main reasons legacy underwriting workbenches have failed is their lack of focus; chimera products mixing administration and underwriting tools sound appealing as a 'single pane of glass' but, based on our conversations with more than 50 clients, have never lived up to expectations. The principal purpose of an agentic underwriting workbench is underwriting.

The agentic underwriting workbench inverts this model. It encapsulates the decision work, performed by agents working under the underwriting team's rules. That includes not just ingestion and triage, but rich pricing logic, underwriting guidelines, and portfolio strategy. The human is no longer the primary operator of the software. The human is the underwriter of record, directing agents and making the calls that require judgment.

Five things differentiate a truly agentic underwriting workbench:

The agents complete actual underwriting work. Not just the currently fashionable tasks of ingestion and triage. They must do the gnarly heavy lifting that leads to a decision - risk assessment, pricing, application of underwriting rules and portfolio strategy - and leave the underwriting team to focus on judgment.

The team's full business logic governs. The agents don't approximate the team's rules - they execute them. This must include nuanced underwriting guidelines and complex pricing algorithms in order to complete the work. The book the team writes is the book the team intended.

Organizational memory compounds. Every override, exception, referral, rationale, and portfolio outcome is signal. That signal accumulates inside the company's own learning loop, not inside someone else's model. It compounds and, over time, swamps the more generic value from LLM outputs.

The system meets the team where they are, not the other way around. The agentic workbench is not a single interface. I know first-hand that lots of underwriting value comes from the moments of judgment that appear in the flow of work. That might be a referral managed via a phone app summarizing the key details, a quick triage approval in Teams keeping the underwriting team in the race for a highly competed risk, or an underwriter and actuary digging into a risk in greater detail on their laptop. Over time, it will also be in the work the team doesn't have to manually oversee - for example, agents working in the background, at night, searching for common underwriting patterns over the course of a renewal season and surfacing them for review.

Humans remain in charge. Authority is tunable at the granularity the team mandates. Approvals can be gated; every action is traceable. Moreover, the system supports a deeply interactive and collaborative interplay between multiple humans and multiple agents as the risk moves through the workflow. The point is not to replace judgment; it's to elevate judgment as the main thing underwriting teams spend their day on.

These are not 'nice-to-haves'; they are essential components of a system that can meaningfully complete underwriting work. This is a new type of technology: a difference in kind, not just degree, from generations before.

Why agentic underwriting workbenches matter

When an underwriting team has a workbench like this, the shape of underwriting changes:

They see portfolio opportunities earlier. With every data point captured and every decision logged, the business can spot shifts in appetite, anti-selection risks, and profitable growth opportunities sooner.

So what? Agents can surface those signals for underwriting leadership before a book has deteriorated, with possible responses to choose from. The workbench does not just support better individual risk decisions; it surfaces better portfolio strategies.

They build compounding decision advantage. Every overridden model output, escalation, and pricing decision that required human judgment becomes reusable institutional knowledge.

So what? The system learns from the expertise of the people using it. Over time, each decision improves the context for the next one, driving better performance, improved consistency, and richer portfolio insights.

They can make more of the book programmable. Historically, algorithmic underwriting was reserved for market segments that could be standardized around common data models and repeatable workflows. Agentic underwriting workbenches make that possible across more risks, and more types of risk. Any submission, regardless of distribution channel or risk type, can be orchestrated by the system, with the underwriter deciding how much agent involvement they need.

So what? That gives the business more flexibility in how it deploys capital: the right underwriting approach for each risk, and better use of the expertise inside the company.

The agentic underwriting workbench does far more than organize tasks; it changes what underwriting teams can see, underwrite, and bind.

First-generation underwriting AI does not make the grade

The last two years have produced a lot of new AI insurtechs, and a lot of underwriting AI. Lots of it has worked: routing is more reliable, submissions are ingested much more quickly, and triage went from wishlist concept to working part of the workflow. None of that is fake; underwriting teams have real efficiency wins to point to.

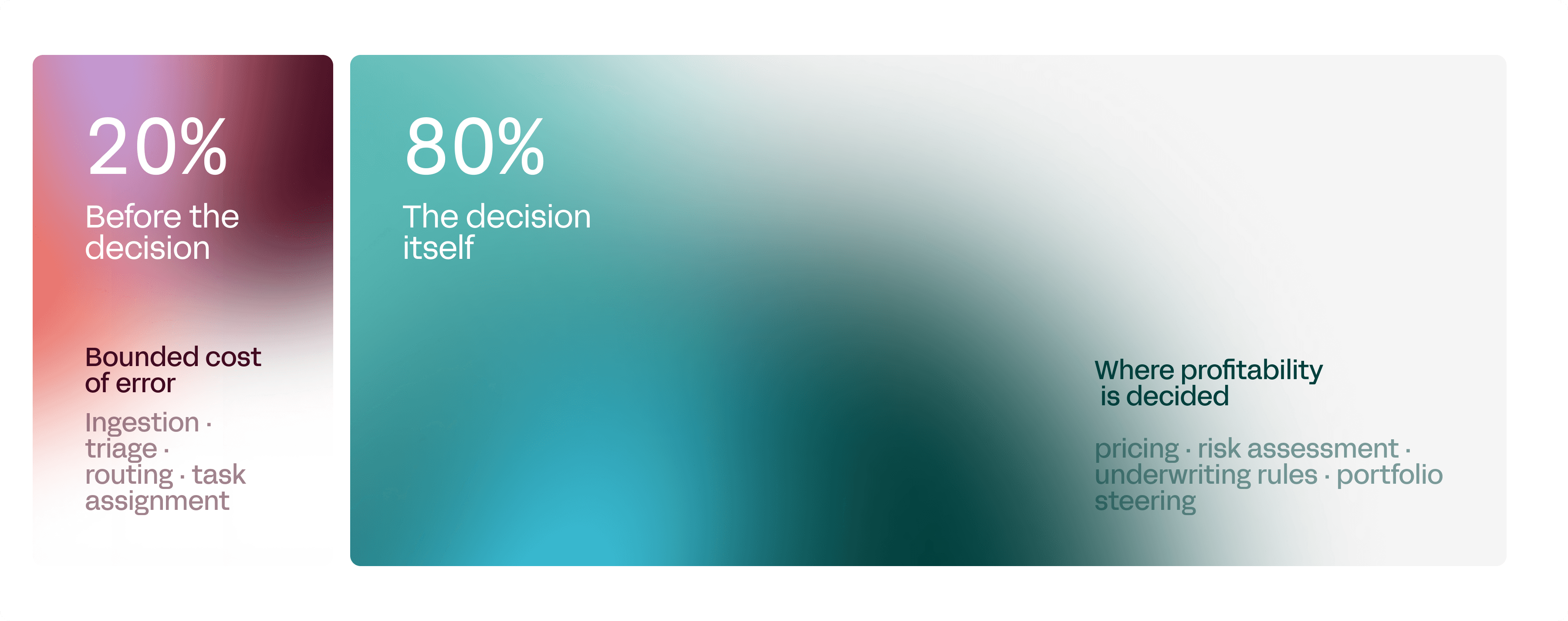

The trouble is that all of those wins are in the first 20% of the workflow.

The 20% is the work that happens before the decision: ingestion, triage, routing, task assignment. It is the part where the cost of error is bounded: the data is structured, and rules of thumb get you most of the way there. The thing is, it's the remaining 80% that's the crux of the problem: pricing, risk assessment, underwriting rules, and portfolio steering. That is what actually drives profitability; I spent more than a decade doing this work as a front-line pricing actuary, so I know it intimately. That 80% requires complex calculations to run, non-obvious underwriting logic to apply, governance to honor, and portfolio-level context to act on. Copilots grafted onto a traditional workbench simply don't have access to this information, and while advancements in LLM integration standards like MCP are meaningful, wiring them in is an art form unto itself (you'll know if you've tried!).

When a company uses AI on the first 20% and stops, two things happen: underwriters move faster (which is important, to be clear), but the underwriting decision gets no better. More insidiously, the business accumulates infrastructure for a category of work that was never the constraint, and none of the infrastructure required for the work that was. There is a reason most of the immature startups out there are attacking the 20% first - it's much easier!

The last cycle proved there is real value in applying AI to underwriting workflows. The opportunity now is to carry that value beyond the first 20%, into the decision itself. The agentic underwriting workbench connects the 20% and the 80% - ingestion to portfolio impact - as one continuous system under the underwriting team's rules.

Nor do the foundation models alone

The other story of the last cycle is that the foundation model has eaten the world. Buyers, executives, and analysts have all been told, loudly, that the model is the product, that the rest is wiring, and that whoever has the best raw intelligence will win the next decade.

There is some truth in some of these statements. LLMs are an unprecedented breakthrough for the world, and their raw capability is staggering. However, it's increasingly clear that in deep specialist domains like insurance, the model itself is the part of the stack that commoditizes fastest. This is playing out right now across the enterprise as clients migrate rapidly to open-weight models in the face of rising costs and, much more worryingly, wanton disrespect for customer data retention, ownership, and privacy by some leading model providers. (That those same model providers are diluting their focus by shifting into many of the industries they serve is a telling sign.)

We can say this plainly because we run on the same frontier models everyone else does. We compare them, we route between them, we benchmark them on real underwriting tasks. We quickly learned two things:

The models are broadly undifferentiated and swappable - there are marginal differences between them, and leaders change places somewhat arbitrarily over time. You only have to look at the way benchmark leaderboards evolve every few months to see proof of this.

The models are not improving quickly - or in some areas at all - when benchmarked on our clients' actual tasks. This is obvious when you think about it: the training data for these models does not contain the domain-specific, nuanced data that is precious and private to our clients. The only way they can absorb it is if the mega-LLM companies appropriate it. It is probably not a coincidence that some of those mega-LLM companies have attempted to dismantle the contracts that prevent this leakage.

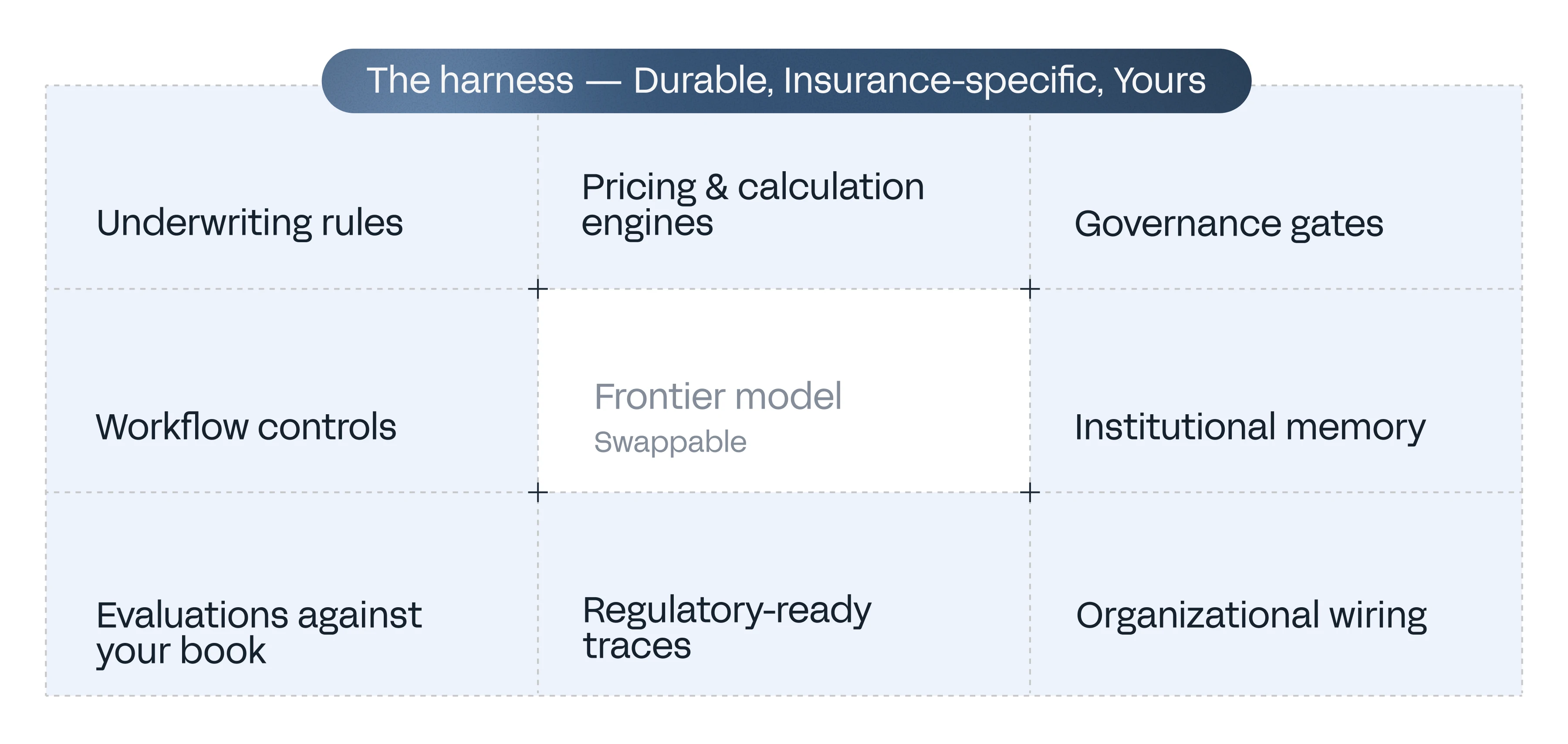

The durable layer is everything surrounding the model: the workflows that safely guide underwriting work forward, the engines that apply your bespoke pricing logic, the governance gates that control each consequential step, the institutional memory of which exceptions you approved last quarter and why, the evals that measure decision quality against your book, and the regulator-ready trace of every action.

The technical community has converged on a word for this layer, the harness, and the data on it has become hard to argue with. The same model, run through a better harness on the same benchmark, jumped from 52.8% to 66.5%.(Footnote 1 ) One team improved their agent's performance by removing 80% of its tools.(Footnote 2) The agent was never the hard part; the harness was. In our industry, where every basis point counts, the gap between a good harness and a bad one can be the gap between a profitable book and a loss-making one.

Raw model capability is like raw underwriting talent: necessary, but it doesn't write a profitable book on its own. The same underwriter performs very differently inside a well-run franchise - clear appetite, good rating models, referral discipline, portfolio feedback - than freelancing alone. The harness is that franchise, built for agents.

In underwriting, the harness must contain the underwriting rules, governance gates, calculation engines, workflow controls, and the client's memory about which decisions worked, alongside more LLM-specific assets like evals and traces. None of that comes from a frontier model contract; none of it can be assembled in a quarter from a generic agent framework. It is years, even decades, of insurance-specific domain decisions and organizational wiring.

A foundation-model agreement gives a client raw intelligence. An agentic underwriting workbench gives a team completed underwriting work. Completed within their underwriting rules, under their controls, with their judgment compounding into firm-wide capability. Those are different products, even when they use the same model underneath.

What this means for underwriting teams

My co-founder Michael and I have spent eight years building toward this category, and more than 20 years envisioning what it means for our clients and industry: a future where underwriters spend more of their day on judgment calls and relationship building, actuaries on improving the models that guide them, and companies on compounding their own decision logic and memory.

Many of the world's most demanding underwriting teams, writing the most complex insurance risks, are already working on this with us. As we approach $100bn of premium per year on our platform, the lessons we've learned from working with our trusted clients are clear: the future of underwriting is simultaneously agentic, client-tailored, and human-led. The underwriting teams that move first will write a better book. The people inside them will do the work their expertise was meant for.

We expect it will be increasingly popular for technology firms to 'go wide', applying their technology to a smorgasbord of loosely related/underwriting-adjacent tasks like FNOL, billing, fraud detection, and other work that's similar in approach, scope, and difficulty to the first 20%. hyperexponential will not do this. We are going all the way for underwriting. It's why we exist.

-

Amrit Santhirasenan is the Co-founder and CEO of hyperexponential (hx), and the host of the Underwriting Intelligence podcast.

Footnotes:

1. LangChain held the model fixed and improved only the harness around it, taking their coding agent from 52.8% to 66.5% on the Terminal-Bench 2.0 benchmark - from outside the top 30 to the top 5. Source: Improving Deep Agents with harness engineering.

2. Vercel cut their internal agent from 15 tools to 2; accuracy rose from 80% to 100%, with 37% fewer tokens. Source: We removed 80% of our agent's tools.